There’s a number. Every parent has one in their head. It’s the projected cost of sending their kid to college, and it’s usually enough to make you wake up in a cold sweat at 3 a.m. For me, it happened when my daughter was about ten. I idly punched some numbers into an online college cost calculator, and the result it spat out was so astronomical, so completely absurd, I actually laughed. Then I felt sick.

That number can feel like a verdict. A financial life sentence. It feels like you’re being told to save an impossible amount of money while also trying to manage a mortgage, car payments, and the ever-rising price of, well, everything. It feels like you have to choose between your child’s future and your own retirement.

So, let’s just get this out of the way. You don’t have to do that. Creating a financial plan for college isn’t about working miracles. It’s about demystifying that terrifying number. It’s about creating a strategy, chipping away at the problem from different angles, and turning panic into a calm, methodical process. It’s a messy, long-term project, but it’s doable. I promise.

Deconstructing the Monster: What ‘Cost’ Even Means

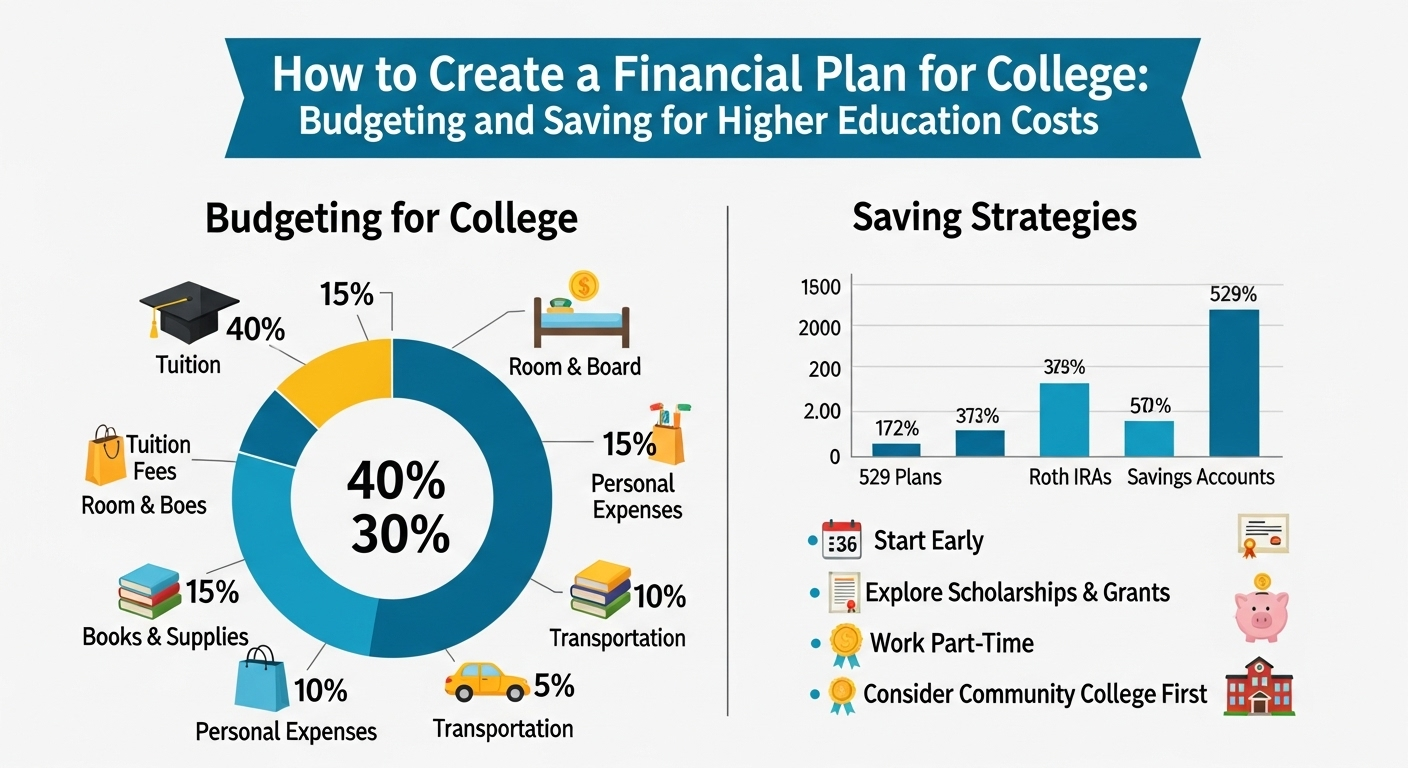

The first thing to do with a scary monster is to turn the lights on. Let’s look at this “cost” thing clearly. It’s not just the tuition fee you see on a university’s website. The total cost of attendance is a four-headed beast:

- Tuition & Fees: The main ticket price. This is what the college charges for the actual education.

- Room & Board: A place to sleep and food to eat. For on-campus students, this is a huge chunk of the cost.

- Books & Supplies: Textbooks can be outrageously expensive. Add in laptops, software, and other materials.

- Personal & Travel Expenses: This is everything else. Flights home for the holidays, a Domino’s pizza on a Tuesday night, going out with friends.

Seeing it all together can make it feel worse, but it’s the necessary first step. I found it helpful to initially ignore the official number and focus on a more empowering one: The Net Price. That’s the total cost minus any grants and scholarships the student might receive. As outlets like Forbes have detailed, very few people actually pay the full sticker price. The goal isn’t necessarily to save the entire amount; the goal is to create a plan to cover the net price.

Your Primary Weapon: The Power of Compounding

If you’re a parent of a young child, you are sitting on a financial superpower: time. The single most effective way to tackle the saving for higher education cost is to start early and let compound interest do the heavy lifting for you. It’s the difference between trying to push a giant boulder up a hill by yourself versus giving it a small nudge at the top and letting gravity take over.

You need a dedicated vehicle for this, not just your regular savings account. In the US, the gold standard is the 529 plan, a tax-advantaged investment account designed specifically for education savings. The money grows tax-free, and you can withdraw it tax-free for qualified education expenses. It’s a phenomenal tool.

If you don’t have access to a 529, the principle is the same. You need a dedicated investment account—perhaps a specific mutual fund—where you can make regular, automated contributions. We’re talking about a Systematic Investment Plan (SIP). This automates your saving, and you get the benefit of dollar-cost averaging. Even a few thousand rupees or a hundred dollars a month, started when a child is five, can grow into a surprisingly large sum over 10-13 years. Tackling a big life goal often requires this kind of long-term vision, a skill you can hone by reading a variety of topics, maybe even at a place like liittlewonder.com.

Shifting Gears: The In-College Budget

Okay, you’ve saved and invested for years. Your kid got in. Amazing. But the financial plan doesn’t stop. It just shifts. Now you move from saving to strategic spending. And this is where your student needs to become part of the team.

Let’s be honest, giving a teenager a lump sum of money for the semester and hoping for the best is not a strategy. It’s a prayer. Before they even step on campus, sit down with them and create a simple college budget. This is less about you controlling them and more about teaching them a life skill. Map it out:

- How much for food beyond the meal plan?

- How much for books? Can you save money by renting or buying used?

- How much for transport?

- How much for entertainment?

Having this conversation sets expectations. It gives them ownership over their financial life. It’s an incredibly important part of their education that they won’t learn in any lecture hall. Mastering a system like this is a mental game, and exploring a range of content on a site like liittlewonder.com can help sharpen those skills.

The journey doesn’t have to be a nightmare. It’s a project. You break it down, use the right tools, and you take it one year at a time.

FAQs: The Real-World Questions Popping Into Your Head

I have a teenager and I haven’t saved anything. Is it hopeless?

It’s not hopeless, but it is urgent. Your strategy has to change. The focus shifts from investment growth to cash-flow planning. How much can you contribute from your current income? What’s a realistic amount for student loans? You’ll also need to double down on searching for scholarships and grants. It’s a tougher road, but far from impossible.

What’s the difference between a scholarship and a grant?

This is a great question. Both are “free money” you don’t have to pay back. Scholarships are typically merit-based—they’re awarded for academic achievement, athletic skill, or other talents. Grants, on the other hand, are typically need-based. They are awarded based on your family’s financial situation.

How much should I even aim to save? The ’50/30/20′ Rule?

There are many rules of thumb, but there’s no single right answer. One common approach is the “one-third” rule: plan to cover one-third of the college costs from savings, one-third from current income during the college years, and one-third through a combination of student loans and financial aid. It’s a balanced approach that makes the savings goal feel less intimidating.

Should my child take on a part-time job at college?

If their academic schedule allows, absolutely. It’s not just about the money, which can be a huge help for covering personal expenses. It’s about the experience. Learning to balance work and study is a powerful life lesson in time management and responsibility.

Is taking out a student loan a sign of failure?

Not at all. For the vast majority of families, student loans are a necessary and strategic part of the overall financial plan. The key is to borrow smartly. Only borrow what you absolutely need, and try to stick to federal loans over private ones, as they often have more favorable terms and repayment options. They are a tool, not a failure.