Isn’t it funny how time and money are connected? When we’re young, we seem to have all the time in the world but no money. As we get older, we might have a bit more money, but time suddenly feels like the most precious commodity of all. This isn’t just a philosophical musing for a lazy Sunday afternoon; it’s the absolute core principle of successful, **long-term investing**.

I was having a chat with my 25-year-old cousin last week. He’s just started his first job, and he’s all fired up, ready to invest in the riskiest, hottest tech stocks, hoping to triple his money by next year. The very next day, I spoke to my 55-year-old uncle, who just sold a property and is now terrified of the stock market, looking to park his money somewhere “completely safe” where it won’t lose a paisa.

Are either of them wrong? No. Not really. They’re just driving on different parts of the same road. And this is the part that so many get wrong—they follow advice meant for someone on a completely different part of the journey. What works for your fresh-out-of-college colleague is likely terrible advice for your nearing-retirement boss.

So, let’s break this down. Forget the complicated jargon. Think of your financial life as a road trip. Your age determines how long you have left to travel, and your **financial goals** are your destination.

Why Your Age is Your Most Important Investment Asset (No, Really)

Here’s the thing. When you’re young, you have a secret superpower: the power of compounding over a long time horizon. Your money doesn’t just grow; the returns on your money also start to grow. It’s like a snowball rolling down a very, very long hill. The longer the hill, the bigger the snowball at the end. That lengthy timeframe allows you to take more risks. If the market crashes (and it will), you have years, even decades, for it to recover. A 28-year-old can afford to see their portfolio drop 20% because history has shown it will likely be much, much higher in 30 years.

This ability to handle volatility is what we call **risk tolerance**. It’s not just about your guts; it’s directly linked to your time horizon. The closer you get to your destination—retirement—the less you want a bumpy ride. You’re no longer looking for adventure; you’re looking to arrive safely with all your luggage intact. This fundamental concept dictates all your **Investment Strategies**.

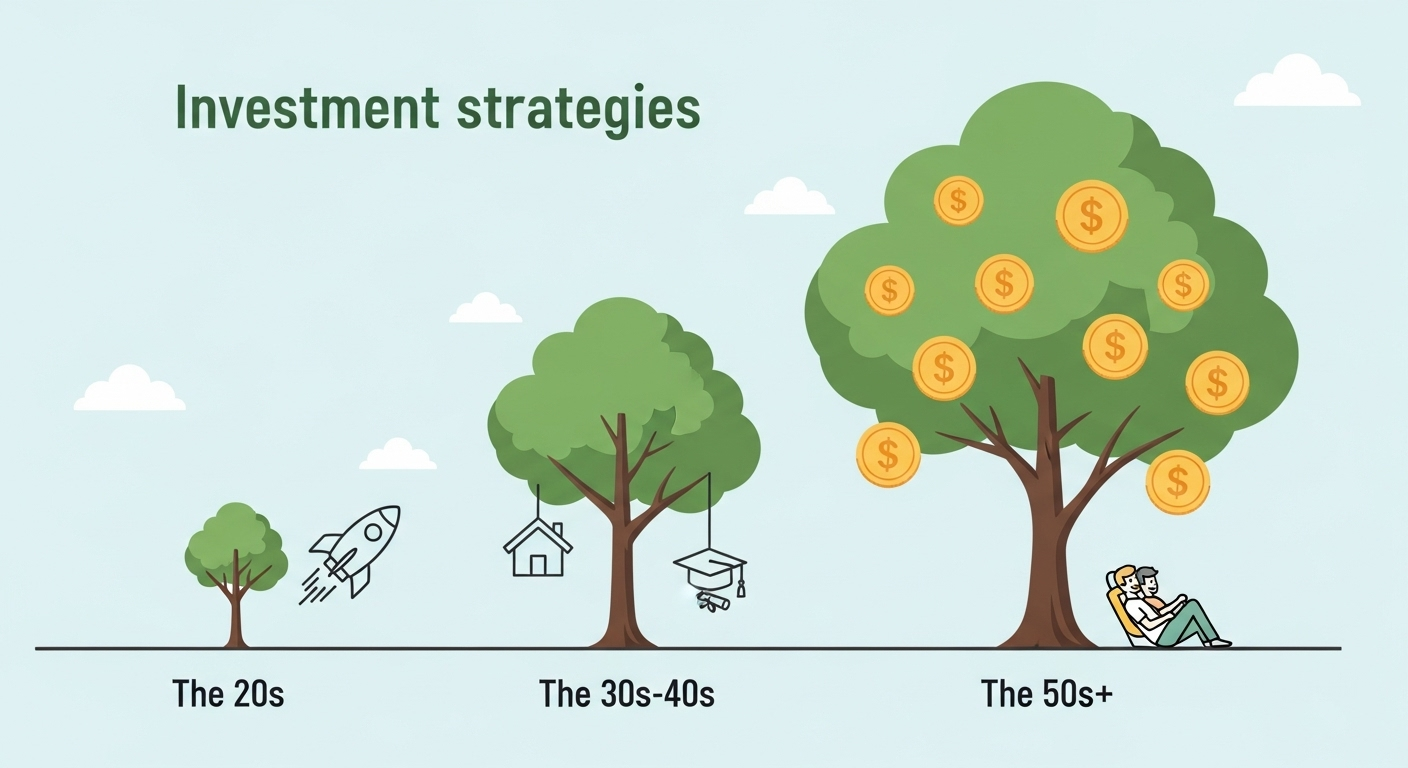

The Roaring 20s & Early 30s: The High-Growth & Accumulation Phase

This is it. This is your high-speed expressway phase. You’re at the start of your road trip with a full tank of gas (time) and minimal baggage (responsibilities). The goal here isn’t just to save; it’s aggressive **wealth creation**.

Your portfolio should be heavily tilted towards high-growth assets. I’m talking mostly about equities (stocks).

- Equities are King: Think about having 80-90% of your investment in equity-related instruments. This could be directly in stocks if you know what you’re doing, or more sensibly for most, through equity mutual funds.

- The Magic of SIP: Start a **Systematic Investment Plan (SIP)** yesterday. Seriously. Drip-feeding a fixed amount into a mutual fund every month is the single most powerful tool for a young investor in India. It automates discipline and averages out your purchase cost over time (something called rupee cost averaging). It’s financial magic.

- Diversify, but Aggressively: Even within equities, spread your money out. A mix of large-cap, mid-cap, and small-cap funds can give you a blend of stability and high growth. Don’t be afraid of the higher risk in mid/small-caps; you have time to ride out the bumps. For more on building smart habits, this guide to personal growth has some interesting parallels.

This is the time to be bold. Your goal is to build the largest possible base for that snowball to grow from.

The Responsible 30s & 40s: The Balancing Act Phase

And then, life happens. You’ve probably added some precious cargo to your car—a spouse, kids, maybe a home loan. The destination is still far away, but you’re driving more cautiously now. Your investment strategy needs to mature with you.

The goal shifts from pure aggression to balanced growth. It’s time to fine-tune your **asset allocation**.

- Start Introducing Debt: It’s time to gently press the brakes. You should start shifting some of your portfolio from pure equity towards debt instruments. Think about an asset allocation of 70% equity and 30% debt. Debt instruments like Public Provident Fund (PPF), Voluntary Provident Fund (VPF), and debt mutual funds provide stability and act as a cushion when the equity market gets turbulent.

- Goal-Based Investing: Your investments now need specific names. This SIP is for the ‘Kids’ Education Fund’ (15 years away). This one is for the ‘Down Payment on a Bigger House’ (7 years away). This helps you choose the right product for the right timeframe. As major news outlets like The Hindu often advise, linking investments to specific goals is a cornerstone of sound financial planning.

- Consider Other Assets: This might be the time you look at other asset classes like real estate or even a small, disciplined allocation to gold (perhaps through Gold ETFs or Sovereign Gold Bonds).

The 50s and Beyond: The Capital Preservation Phase

You can see the destination on the GPS now. The hotel for your **retirement planning** is just a few exits away. Your absolute priority is to not get into an accident and lose what you’ve spent decades building. The name of the game is no longer wealth creation; it’s wealth preservation.

It’s time for a major strategic shift towards stable, income-generating assets.

- Equity Takes a Back Seat: Your asset allocation should flip dramatically. You might be looking at 60-70% in debt and only 30-40% in equity. That equity portion is still important to beat inflation, but it’s no longer the engine of your portfolio.

- Focus on Fixed Income: This is where traditional, ‘safe’ investments shine. Senior Citizen Savings Scheme (SCSS), Post Office Monthly Income Scheme (POMIS), and high-quality bond funds should form the core of your portfolio. The goal is a predictable, steady stream of income.

- Systematic Withdrawal Plan (SWP): Just as SIPs were magical for building wealth, SWPs are the tool for carefully withdrawing it. It’s the reverse of a SIP, providing you with a regular pension from your mutual fund corpus. Check out another insightful piece on long-term goals at liittlewonder.com.

Let me try to put this another way. In your 20s, your money is a soldier sent to conquer new territory. In your 50s, your money is a guard tasked with defending the fortress you’ve already built.

FAQs That People Genuinely Ask

Wait, so if I turn 50, do I have to sell all my stocks overnight?

Absolutely not! This is a gradual process, not an on/off switch. You should start rebalancing your portfolio gradually as you move through life stages. Think of it as slowly easing your foot off the accelerator and onto the brake over several years, not slamming on the brakes at your 50th birthday party.

What is a SIP exactly and why is everyone obsessed with it in India?

A SIP, or Systematic Investment Plan, is simply a standing instruction to your bank to invest a fixed amount of money into a specific mutual fund every month. It’s popular because it forces discipline (you invest without thinking about it) and helps manage market volatility through rupee cost averaging—you buy more units when the market is low and fewer when it’s high. It’s the simplest way for a common person to participate in the stock market’s long-term growth story.

My risk tolerance is high even though I’m in my 40s. Should I still shift to debt?

That’s a great question. Your personal risk tolerance absolutely matters. If you have a very stable, high income and a strong stomach for volatility, you could maintain a higher equity allocation than your peers. However, you should still acknowledge your time horizon. While your personal tolerance might be high, your *time* to recover from a major market downturn is shrinking. A little balancing is always prudent.

How often should I review and change my investment strategy?

You shouldn’t be tinkering with it every month. A good practice is to review your portfolio once a year. Check if your asset allocation is still aligned with your strategy. For example, if a great year for stocks meant your equity allocation swelled from 70% to 80% of your portfolio, your annual review is the time to rebalance it by selling some equity and buying debt to get back to your target allocation.