I still remember my first ‘real’ job. The one that came with a proper offer letter and a salary that felt, at the time, astronomical. I remember getting that first payslip, looking at the number, and thinking, “I’ve made it. I’m basically a mini-Mittal.” The next thought, of course, was far more terrifying: “…what on earth do I do with this money?”

Sound familiar? That moment is the starting line of a financial marathon. And here’s the problem: most of the advice out there treats this marathon like a 100-metre dash. They yell “SIP! Equity! Mutual Funds!” without asking you the most important question: “Where are you in the race?” Because the strategy you use in the first 5 kilometres is wildly different from the one you need when the finish line is in sight.

Thinking you can use the same investment strategy your whole life is like a cricketer deciding he’s only ever going to play the cover drive. It might be brilliant sometimes, but in other situations, it’s going to get you out. The truth? Your financial life has seasons. And you need to dress appropriately for each one. So let’s ditch the generic advice and talk about what investing *really* looks like as life happens.

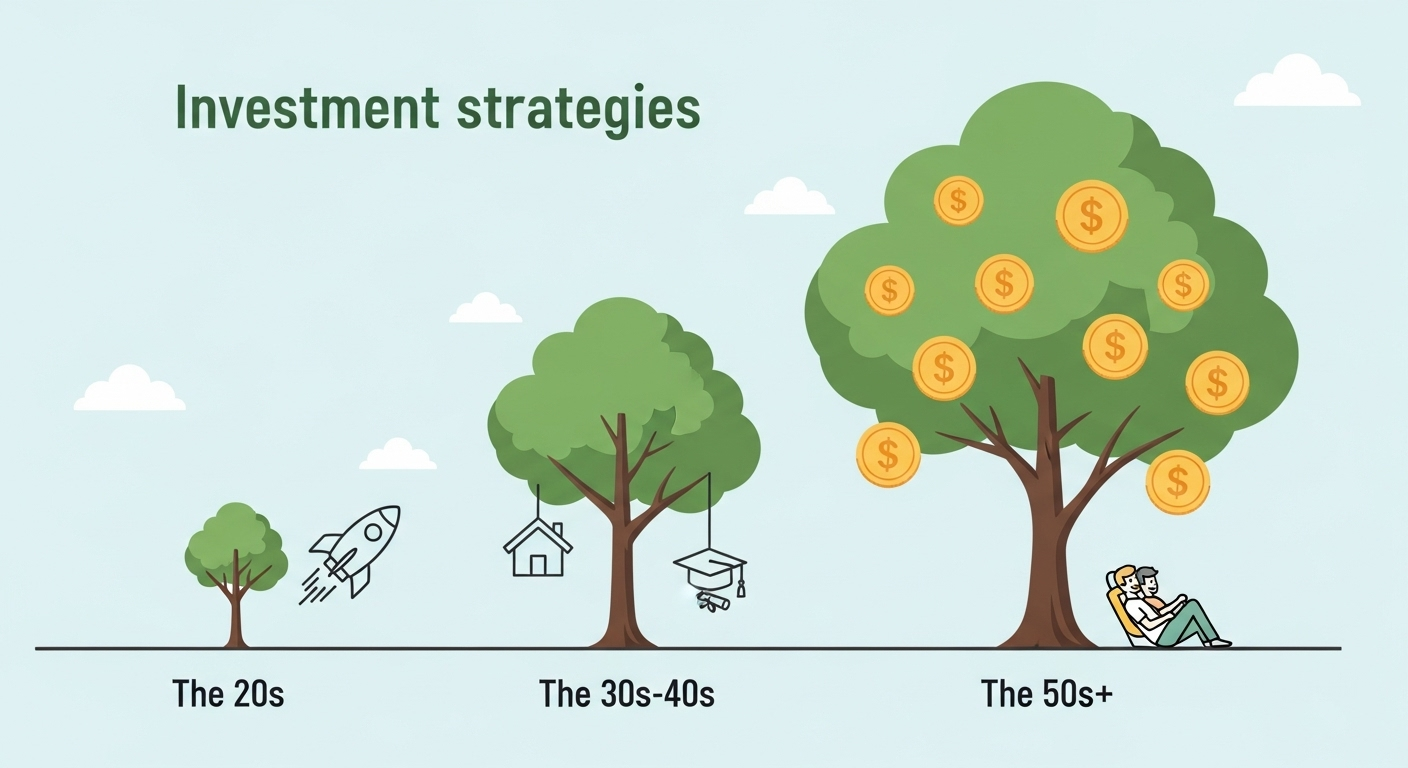

The Roaring Twenties: Your Golden Ticket is Time

Ah, your 20s. You have less money, probably a mountain of student debt if you’re like I was, but you are sitting on an absolute goldmine. That goldmine is Time. And thanks to the eighth wonder of the world—compound interest—time is the most powerful ingredient in any investment recipe.

Let me put it this way. Compounding is like a tiny snowball at the top of a very, very long hill. The longer the hill, the bigger the snowball gets by the time it reaches the bottom. Your 20s are the top of that hill. The small amounts you invest now have 30, 40, or even 50 years to roll and gather more snow. It’s actual magic. This is why the best investment for beginners in India often starts with just a small, consistent amount.

So, what’s the game plan?

Your mantra is: Growth. Your biggest asset is your ability to take risks because you have decades to recover from any market downturns. This is the time for a heavy allocation to equities, primarily through SIPs in good equity mutual funds. Don’t get scared by market volatility. See it as a sale—you’re buying more units when the price is low. You’re building the foundation for your future self, and it needs to be aggressive. A little bit of learning about the market now can be invaluable, a concept explored in different ways at Liittle Wonder.

The Squeezed Middle: The 30s & 40s Juggling Act

And then, life gets… complicated. The 30s and 40s. The ‘settling down’ years. Suddenly, you’re not just investing for some abstract future. You’re saving for very real, very specific things. A down payment for a house. Your kids’ ridiculously expensive education. A bigger car. And oh yeah, that thing called retirement is starting to look less like a blurry dot on the horizon and more like an approaching train.

I initially thought this was the time to slow down, but actually, that’s not quite right. It’s the time to get smarter. Your mantra shifts from pure growth to goal-based investing.

This means you can’t have one big pot of money anymore. You need different buckets for different goals.

- Long-Term Bucket (Retirement): This still needs to be aggressive and equity-heavy. Don’t pull your foot off the accelerator here. Keep those SIPs going. This is the core of your retirement planning India strategy.

- Medium-Term Bucket (5-7 years, e.g., House Down Payment): This needs to be more balanced. You can’t afford a huge market crash right before you need the cash. This is where hybrid funds (a mix of equity and debt) or even debt mutual funds come into play.

- Short-Term Bucket (1-3 years, e.g., Car Purchase): This needs to be safe. Think liquid funds or fixed deposits. You’re not trying to grow this money; you’re trying to preserve it.

This is also the stage where you start looking at diversifying. Maybe a piece of real estate, if that aligns with your goals. The key is to match your investment’s risk and timeline to the specific goal it’s meant for. It’s a juggling act, for sure, but it’s a manageable one. It’s all about meeting your financial goals, a topic news outlets like NDTV often cover in their personal finance segments.

The Home Stretch: Protecting Your Nest Egg in Your 50s & Beyond

You’ve run most of the race. The finish line is visible. The absolute last thing you want to do now is trip and fall. The entire focus of your investment strategies for different life stages shifts dramatically here. The game is no longer about growing your wealth aggressively.

Your new mantra is: Wealth Preservation.

Your goal is to protect the capital you’ve spent a lifetime building and make it generate a steady income to live on. A massive market crash could be devastating at this stage because you don’t have time on your side to recover. This means systematically moving your money from high-risk equity to lower-risk debt instruments.

I keep coming back to this point because it’s crucial: The risk that served you so well in your 20s is now your enemy.

This is where instruments like the Senior Citizens’ Savings Scheme (SCSS), Post Office Monthly Income Scheme (POMIS), and other fixed-income avenues become your best friends. Your portfolio, which was maybe 80% equity in your 20s, might now be 70% or 80% debt. It’s about turning your pile of money into a reliable paycheck for your retirement years. It might feel boring compared to the thrill of the stock market, but believe me, the peace of mind it brings is anything but boring. Exploring different ways to stay sharp and strategic is always a good idea, even checking out varied content on sites like liittlewonder.com can keep your mind active.

FAQs: The Things You’re Actually Wondering

I’m in my 40s and haven’t started investing properly. Is it too late?

Absolutely not! Is it harder? Yes. Do you have less time for compounding to work its magic? Also yes. But is it too late? Never. The best time to start was