Let’s start with a truth that feels a bit uncomfortable. A business partnership is a lot like a marriage. There’s the initial excitement, the shared dreams, the late-night brainstorming sessions that feel electric. You’ve found someone who gets your vision. You’re ready to conquer the world together.

But just like a marriage, the number one thing that can tear a great partnership apart isn’t a bad business idea or a tough market. It’s money.

I’ve seen it happen. Friends who were inseparable, who started a brilliant cafe together, ended up not speaking to each other because of a dispute over who should get a bigger share of the profits. It’s heartbreaking. The frustrating thing is that most of these problems are completely avoidable. They don’t start from a place of greed, but from a place of ambiguity. From conversations that were never had.

So, before you print those business cards, let’s have a real chat. A coffee shop chat. Let’s talk about the financial foundations you absolutely must lay to give your partnership the best possible chance of not just surviving, but thriving.

The Business Prenup: Your Partnership Deed Is Not Just Paper

You wouldn’t get married without talking about the future, right? A partnership deed is your financial prenuptial agreement. And yet, so many new partners either skip it, or download a generic template and sign it without a second thought. This is the single biggest mistake you can make.

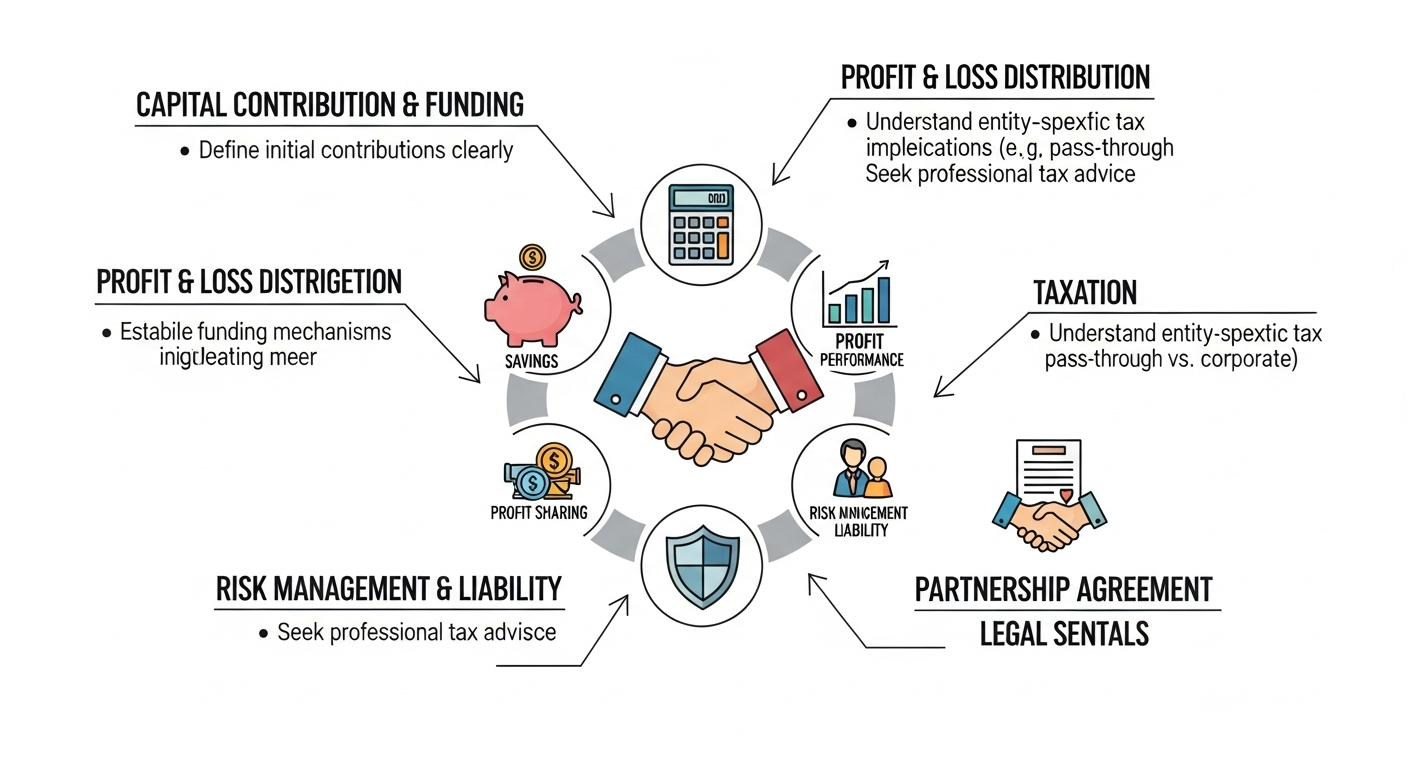

Let me be brutally honest about this: a vague partnership deed is a ticking time bomb. It needs to be a detailed, custom-made document that outlines every single financial aspect of your business relationship. You need to sit down with your partner and a good lawyer and hash out the tough questions *now*, while you’re still excited and on the same team. Specifically, it must cover:

Capital Contributions. Who is putting in what? Is it just cash? Is one partner contributing equipment, a client list, or their expertise? Assign a clear, agreed-upon value to these non-cash contributions. How and when will this capital be returned, if ever?

The Profit (and Loss) Sharing Ratio. Don’t just assume it’s 50/50. What if one partner is working full-time and the other is part-time? What if one has more experience and is expected to bring in more business? The profit sharing ratio should reflect the value and effort each partner brings. And don’t forget losses. How will you share those? Answering this now prevents a world of resentment later.

Salaries and Drawings. Are you going to pay yourselves a fixed monthly salary? Or will you take ‘drawings’ from the profits when the business has cash to spare? A fixed salary provides predictability for your personal finances, while drawings offer more flexibility for the business. There is no right answer, but there has to be *an* answer. An agreed-upon one.

The Exit Strategy. This is the clause everyone ignores, but it’s arguably the most important. What happens if one partner wants to leave, becomes incapacitated, or sadly, passes away? How do you value their share of the business? Does the remaining partner have the first right to buy them out? How will that buyout be funded? Thinking about the end, at the beginning, is the most mature thing you can do for your business.

One Pot is a Bad Pot: Managing the Money Day-to-Day

Once the deed is signed, the real work begins. And the second biggest mistake I see partners make is mixing funds. Using personal bank accounts for business expenses, or one partner’s account as the main business account. It’s a disaster waiting to happen.

A Separate Business Bank Account Is Non-Negotiable

The very first thing you do, after registering your partnership firm, is to open a dedicated business bank account. In India, this will be a current account in the name of the partnership. All money earned by the business goes into this account. All business expenses are paid from this account. This creates a clean, transparent financial record. It’s not ‘your money’ or ‘my money’ anymore. It’s ‘the business’s money’. This simple act professionalizes your operation overnight and makes accounting a million times easier.

Keep Track of Everything. Religiously.

Use an accounting software. Hire a part-time accountant. Use a detailed spreadsheet. I don’t care what you use, but you must track every single rupee. This transparency builds trust. It means that at any point, both partners can see exactly where the money is coming from and where it’s going. This prevents suspicion and misunderstanding. To dive deeper into smart operational habits, check out some of the great articles on Liittle Wonder.

Have Regular Money Meetings

Set aside time every month, or at least every quarter, to review the financials together. This shouldn’t be a tense, confrontational meeting. It’s a business review. How are the sales? Are expenses higher than expected? Do we have enough cash flow for the next few months? Making this a routine part of your business keeps you both aligned and turns financial discussions into a normal, strategic process, rather than a fight. As leading financial news sources like Reuters often show, consistent financial oversight is a hallmark of successful companies.

Thinking Bigger: Profits, Taxes, and Growth

So you’re making money. Fantastic! Now what? The next set of financial decisions revolves around growth and compliance.

Decide how much profit to reinvest back into the business. Do you upgra